Targeting the full value of digital disruption through business model innovation

Dr Chander Velu, head of the IfM’s Business Model Innovation research group, has been collaborating with digital strategy consultants at IBM to consider how the next wave of digital technologies will impact on firm-level business operations, and to create a framework for companies to target the full value potential including the implications for business models. We interview Chander to find out more about the research…

Your research identifies a ‘second wave’ of digital disruption. What is meant by the second wave?

Over the past few years we’ve seen widespread disruption driven by new technologies which have revolutionised the way companies can interact, including within their organisations, with their supply chain partners, and with their customers. This disruption has included e-commerce, and has been centred on internet-enabled platforms.

As part of this first wave, advancements in mobile, cloud and analytics have resulted in the rapid expansion of digital platforms and more personalisation of offers. The platform companies that emerged from this shift captured significant value by monetising direct access to the customer. Many have also created new value through external networks, often by acting as intermediaries within ecosystems.

So what’s changing to indicate a ‘second wave’? Well, the maturity of cloud, analytics and mobile is now matched with the progress in Internet of Things (IoT), artificial intelligence (AI) and blockchain technologies. New digital technologies are creating intelligent engines that enable augmented human intelligence, autonomous decision making, more efficient machine-to-human interactions, and optimisation of any system in real time.

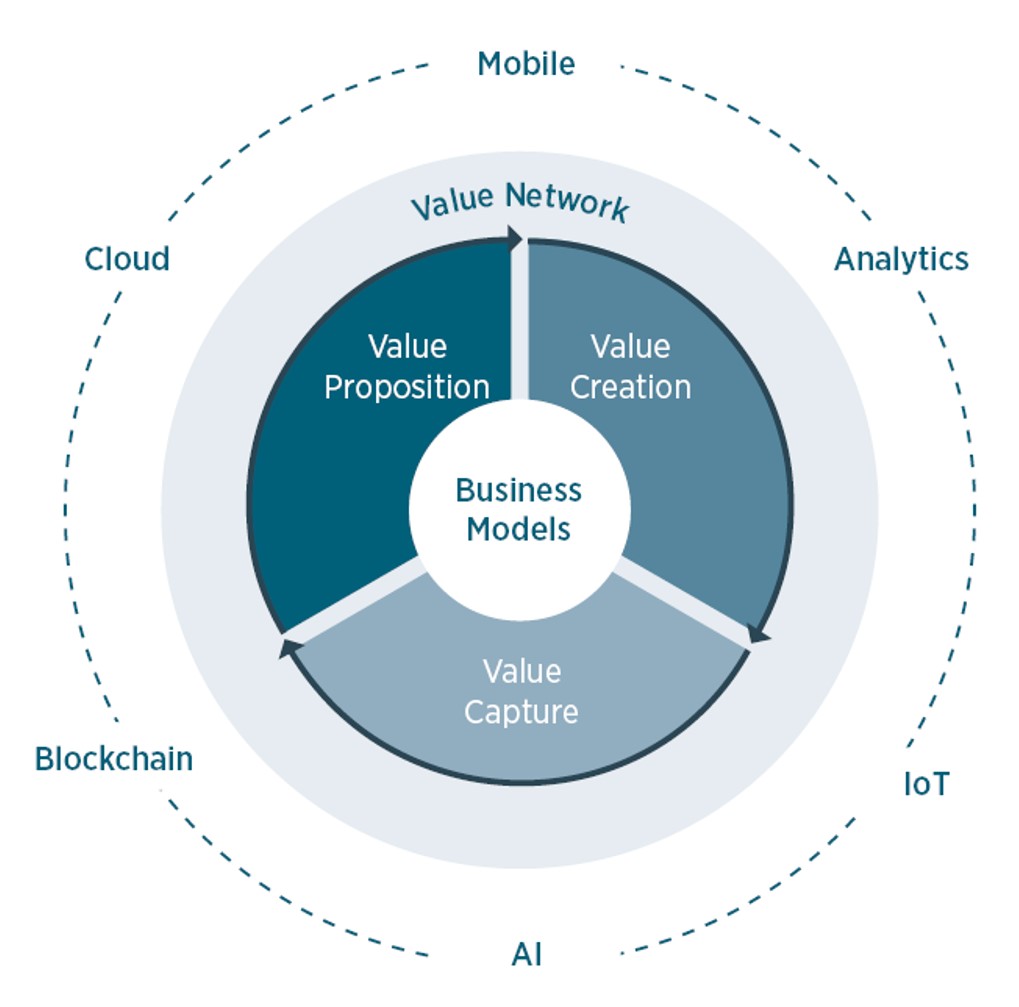

Collectively, these newly emerged technologies are changing the economics of industry value chains from end-to-end and are impacting every component of business models – the value proposition, value creation, value capture, and value network (see Figure 1).

Figure 1: Business model components - 4Vs

Source: Velu, C; Coopetition and Business Models, Routledge (2018)

These technologies can enable new value propositions, capabilities, and optimisation opportunities in end-to-end supply chains, operations and distribution. Yet at the same time they are causing significant changes in how organisations position themselves, as well as dislocation and disintermediation of players in the value chain through the emergence of new business models.

Can you share some examples from industry?

There are some great examples showing how digital technologies are resulting in innovative business models through extended value networks, and how these can render some business models and players in the value chain irrelevant.

The Food Trust blockchain is an example of an industry partnership that improves transparency and efficiency across the entire food supply chain. This ecosystem includes retailers (including Walmart, Kroger, Dole, Nestle, Tyson Foods and Unilever) growers, distributors and more, who collaborate to improve food safety by pinpointing contamination sources. Walmart is now able to trace food-based products back to the original source within 2.2 seconds. Each new supplier or distributor entering the Food Trust creates more value for all members; suppliers get access to a broader network of consistent demand and distributors get access to a larger variety of supplies with diminishing costs.

Such industry partnerships and coopetition business models, whereby competing firms cooperate, are emerging across more and more industries. The rationale for coopetition-based business models could be to increase the size of the current market, to create new markets, or to increase efficiency in resource utilisation in order to help improve the firms’ competitive position.

Another example shows the cost of being left behind with a business model that has been superseded: American Tire Distributors, the largest distributor of tyres in the US, filed for bankruptcy in 2018. Their position in the value chain was disintermediated after the two of the largest tyre manufacturers in the US (Goodyear and Bridgestone) decided to go directly to consumers through their own networks, and Sears Holdings Corp. agreed a partnership to install tyres bought on Amazon.com.

What are the challenges of estimating and measuring the value of digital initiatives? And what is the ‘productivity paradox’?

Assessing the value and impact from digital technology investments remains a challenge for most enterprises.

For businesses, improved profitability and productivity are often used to measure the impact of digital initiatives. Digital technologies can increase profitability by reducing a wide range of costs across the value chain. These technologies are streamlining supply chain activities through integration, automation, tracking and better forecasting. They are also driving significant operational efficiencies through more efficient use of equipment, increased labour productivity, and enhanced monitoring and management. In distribution, they help remove steps and activities between customers and how they use goods and services.

Productivity, however, presents a conundrum. In spite of the prevalence of digital technologies, in aggregate there seems to be a persistent slowdown in productivity that has plagued modern economies for the past 10 years. This is widely known as the ‘productivity paradox’ and there are many possible reasons that explain it. These include the impact of the financial crisis, the lack of diffusion of the benefits of digital technologies among small and medium sized enterprises, mismeasurement of the digital economy, and more.

However, our view is that siloed approaches, too much focus on operational efficiencies, and the lack of business model innovation following the adoption of digital technologies, could also be major contributors to the productivity paradox.

How can firms capitalise on the opportunities opening up from this second wave of disruption?

Firms are approaching digital initiatives in one of two ways. The first is a primary focus on incremental product improvements and operational efficiencies. Most digital initiatives fall into this first category. This is likely because firms can see the results of such initiatives faster and can use wellestablished

cost take-out KPIs to set targets and measure success. The impact from these cost savings and productivity gains will be significant. We estimate that in the US alone this will amount to an average of USD 1.8 trillion per year over the next 10 years. However, these efficiency gains represent only a portion of the value potential and will not be evenly distributed across sectors.

Indeed, the second category of digital initiative offers much more extensive potential value, and the development of new value propositions could contribute to significant growth and innovation through the design of new business models. The combination of IoT, AI and blockchain, in particular, could enable strong network effects, whereby an established leader can drive a virtual circle of adoption resulting in improved capabilities and economics. As such, it is imperative for organisations to assess value creation and capture opportunities through expanded value networks.

How have you estimated the potential value of emerging technologies in your research?

To estimate the potential impacts of five core digital technologies (mobile, cloud/analytics, IoT, cognitive/AI, blockchain), we developed a value chain-based model. We estimated total impacts by cataloguing how each technology could transform individual parts of each sector’s value chain. We assessed current and planned uses of emerging technologies for leading firms in each sector.

We then mapped where in the value chain these technologies were being applied, and how they would create value, and documented any publicly disclosed estimates of the potential or already delivered value. The full encyclopedia of unique use cases documents over 200 distinct applications.

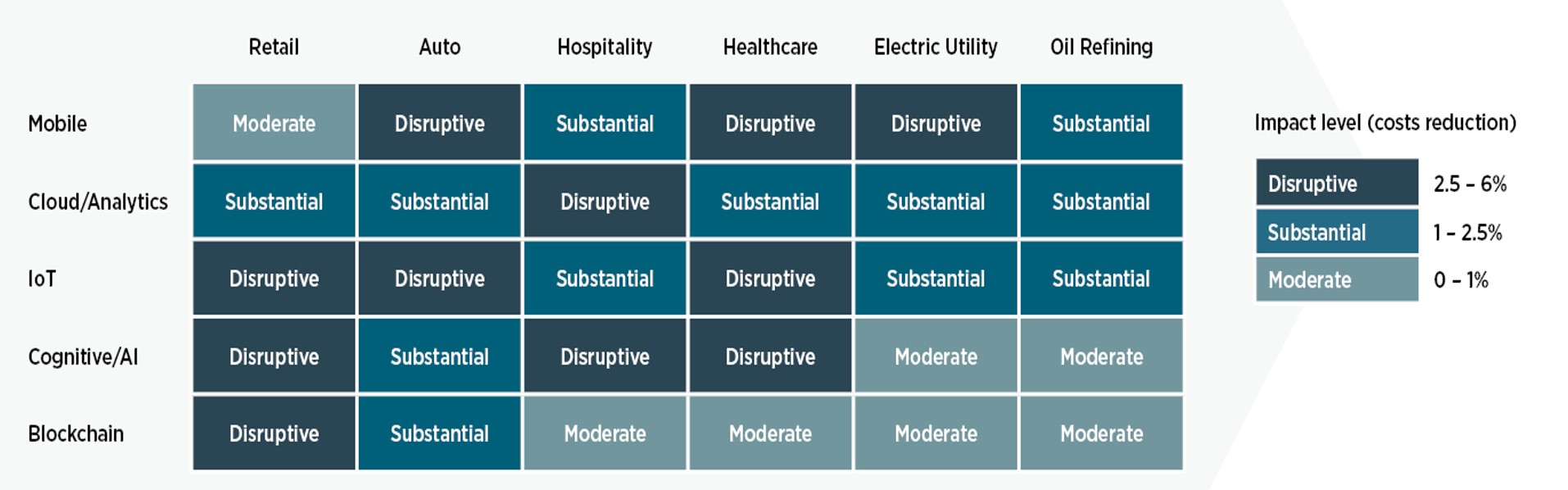

While emerging technologies will impact all sectors, the value they create will not be evenly distributed. The amount of impact depends on a variety of factors including, but not limited to, which parts of the value chain are affected, which technologies dominate, and the speed with which different industries drive successful adoption of digital technologies. We have done a ‘bottom-up’ estimate on several sectors in order to see how different the impact could actually be (see Figure 2).

Figure 2: Estimated technology impact potential by industry sector

Source: IBM and Cambridge research and analysis

What strategic approaches can be used to target the potential value of digital transformation?

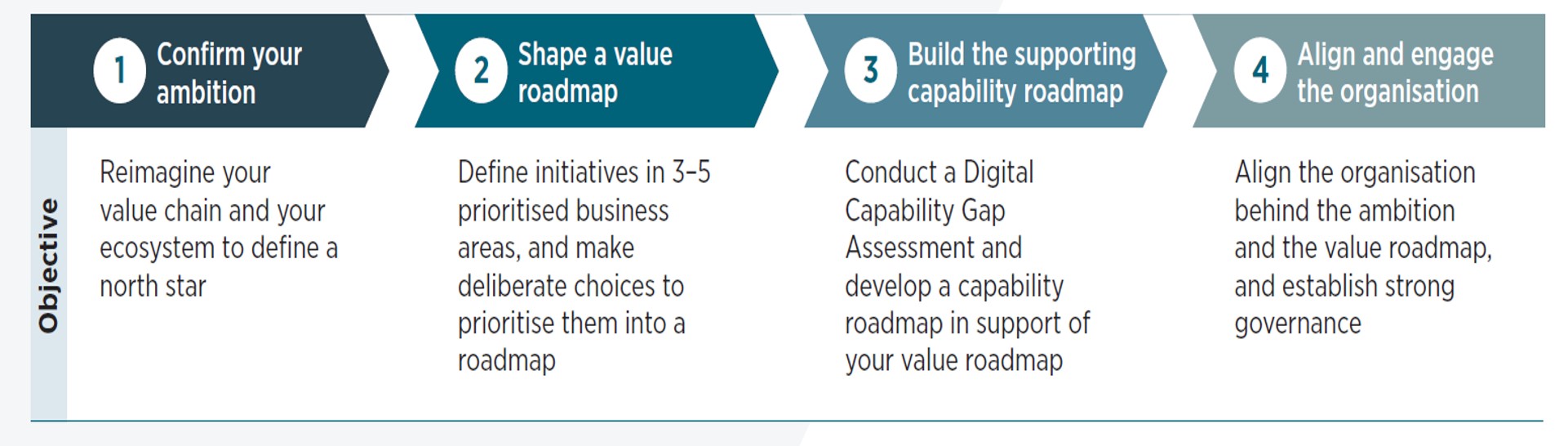

From our research on digital business model innovation, and drawing on experiences of managing digital transformation efforts, we have developed practical recommendations for how to increase the likelihood that digital transformation efforts are successful in targeting the full value potential.

These focus on four courses of action (shown in Figure 3):

- Confirm your organisational ambition by mapping and reimagining your ecosystem and your value chain.

- Identify opportunities and define initiatives across every component of the business model and make deliberate choices in prioritising them into a value roadmap.

- Conduct a digital capability assessment to develop a capability roadmap in support of the value roadmap.

- Align and engage the organisation behind the ambition and the value roadmap; shape a programme with strong governance.

Figure 3: Four courses of action to target potential value

Ultimately, the firms best placed to reap the opportunities presented by the second wave of digital disruption will be those who can identify value opportunities, and create and capture the value from them based on the ability to adapt and configure their own capabilities and their strategic partnerships. This will rely on adopting a structured approach to business strategy, developing the skills and capabilities required, and building technological solutions which deliver customer needs more effectively than competitors. A company’s willingness to innovate and change its business model will be fundamental.

For further information please contact:

Dr Chander Velu